Primary documents: act of reconciliation of mutual settlements

Reconciliation report of mutual settlements- one of the primary accounting documents.

The essence of such a document is to record at a certain moment the state of mutual settlements between two counterparties.

Thus, a reconciliation act can be signed between the buyer and the supplier, the payer and the Pension Fund, between two enterprises of the same holding company, and even between two structural divisions of the same enterprise.

The reasons for signing the reconciliation report include the following:

- long-term cooperation between two counterparties;

- the possibility of deferring payment for goods;

- when an enterprise works with a wide range of goods;

- when goods are of very high value;

- inventory of the state of mutual settlements with counterparties;

- the need to confirm accounts receivable or payable to regulatory authorities or senior management, etc.

The act of reconciliation of mutual settlements can be drawn up for a month, quarter, year or even for the entire period of work. There are no strict requirements for its design or frequency. The only thing that needs to be observed when drawing up this document is the separation of data according to contracts.

For example, if the same organization acts as a buyer for some goods and a supplier for other goods, then it is better to make two reconciliation reports, separately for accounts payable (and the corresponding supply agreement), and separately for accounts receivable.

Drawing up a reconciliation report for mutual settlements

The legislation does not establish uniform rules for drawing up and issuing a reconciliation report, however, there are basic principles that must be followed. Like any primary document, the reconciliation report must contain the following mandatory details:

- the name of the document, as well as the date of its preparation;

- the name of the originator’s organization and the name of the counterparty with whom the act is signed;

- indication of officials authorized to sign acts of verification of their surnames and initials, as well as signatures.

The reconciliation act itself is usually drawn up in the form of a register of documents, ordered by the date of their creation. Sometimes, instead of documents, the essence of the transaction is indicated (sale, purchase, payment, etc.).

In order for the reconciliation act to be up-to-date, it is better to draw it up from the beginning of cooperation or from the moment of signing the last reconciliation act. In addition to the originator, this document must be signed by the director of the enterprise.

The original reconciliation act, signed by the directors of the counterparty enterprises and certified by their wet seals, has legal force.

Signing the reconciliation act and its legal force

Remember that the counterparty (especially your debtor) may refuse to sign the reconciliation report, and you will not be able to legally influence his decision. Therefore, it is worth stipulating the mandatory reconciliation of mutual settlements and the periodic signing of relevant acts in the contract, indicating the timing and procedure for such reconciliation. It is also worth providing for liability for refusal or evasion of reconciliation.

When resolving disputes, judges have repeatedly expressed the opinion that the reconciliation act is not unambiguous evidence of existing debt, but it can be a good reinforcement of the available primary documents confirming its existence.

Also, a signed reconciliation act allows you to “push back” the statute of limitations. The new limitation period is counted from the date of signing the act, regardless of the date of the controversial transaction itself.

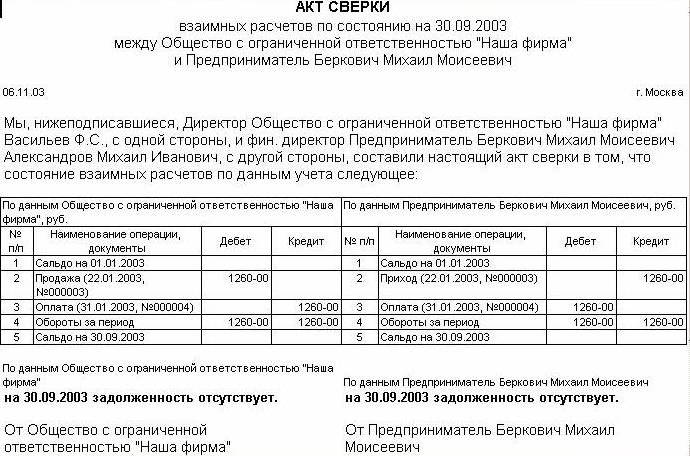

Sample of filling out a reconciliation report for mutual settlements

Reconciliation report form

You can download a blank form for the mutual settlements reconciliation report for Excel at