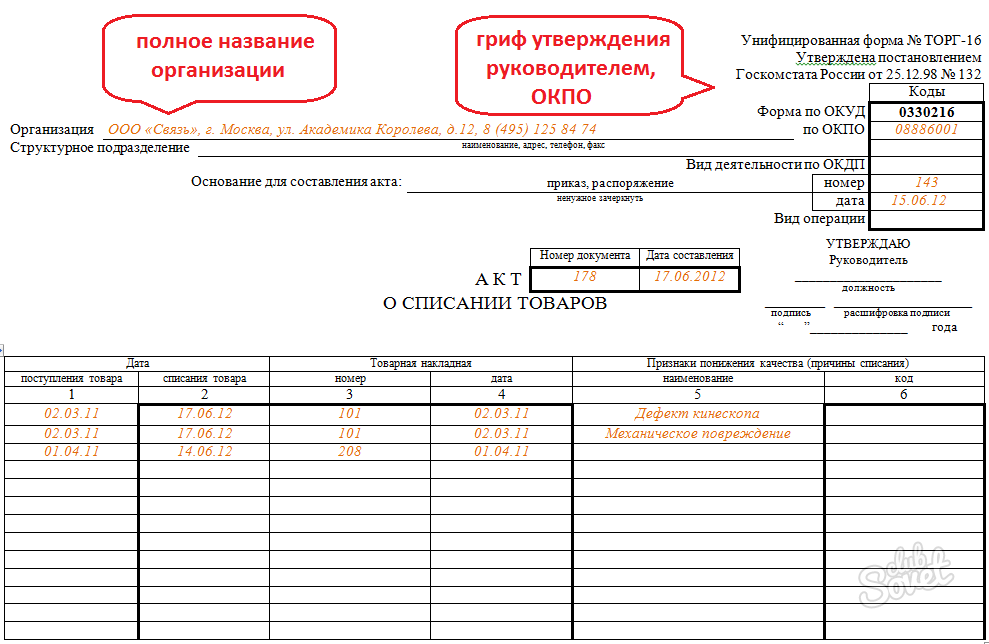

Inventory-material assets (TMC), which are the property of the enterprise, may eventually become unusable and must be written off. The reason for write-off can be damage, expiration, theft. In order to document the fact of write-off, an act of write-off of goods is drawn up in the established form TORG-16, approved by the State Statistics Committee of the Russian Federation on December 25, 1998 by resolution No. 132.

If the goods cannot be used at the enterprise or sold as a result of loss of quality, marriage, breakdown, then a write-off certificate is drawn up in the form TORG-16. There is no single established form for writing off for other reasons (the goods are morally obsolete, the depreciation period has ended). Currently, write-offs for other reasons are drawn up in an arbitrary form developed at the enterprise, taking into account the office work standards adopted at it. Before writing off, an inventory of goods is necessary. Its result is an inventory in the INV-3 form.

Documents for download:

A commission is collected to assess the condition of the goods. Its composition may change over time or remain constant. The commission must include the head of the organization, the chief accountant, employees materially responsible for the write-off object, specialists in the profile of work related to the use of equipment to be written off. The head of the enterprise approves the composition of the commission and issues an order based on the write-off act.

At the beginning of the write-off act, it is obligatory on the first page in the upper right corner that the stamp of approval of the write-off act by the head of the enterprise is placed. On the left, all the details of the organization are recorded: its name, administration, code of the structural unit that writes off inventory, OKPO code, full name of the materially responsible person.

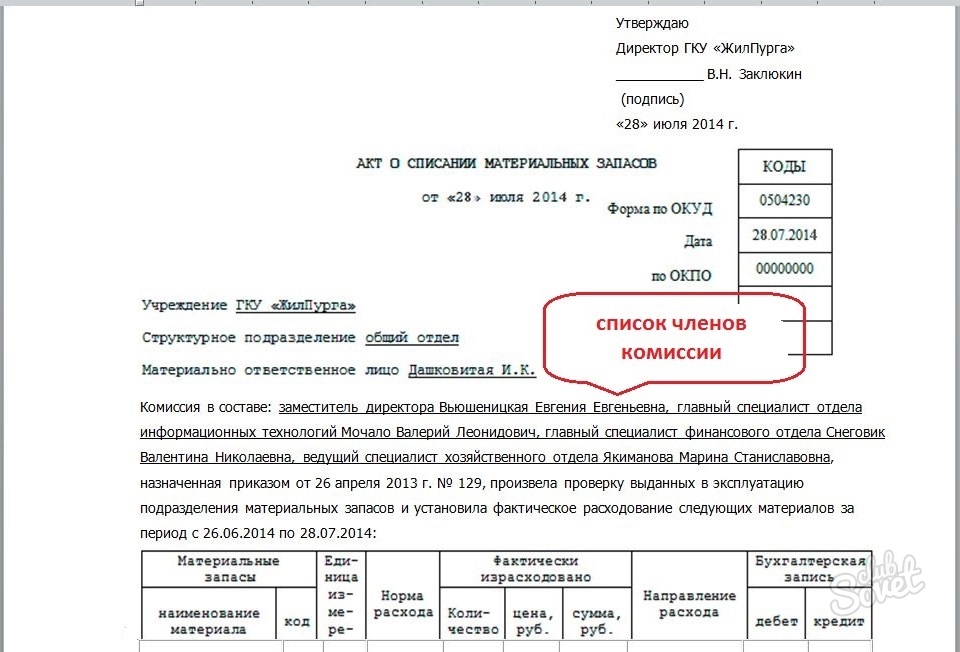

Mandatory part of the act is the date and place of manufacture. They follow the name of the act. It also records the basis for the action of the commission, the number, date of publication of the order, certified by the head. The next part of the document is a list of committee members for the write-off process. The full name of the chairman is written first, then the remaining members of the commission are listed in alphabetical order, indicating their position.

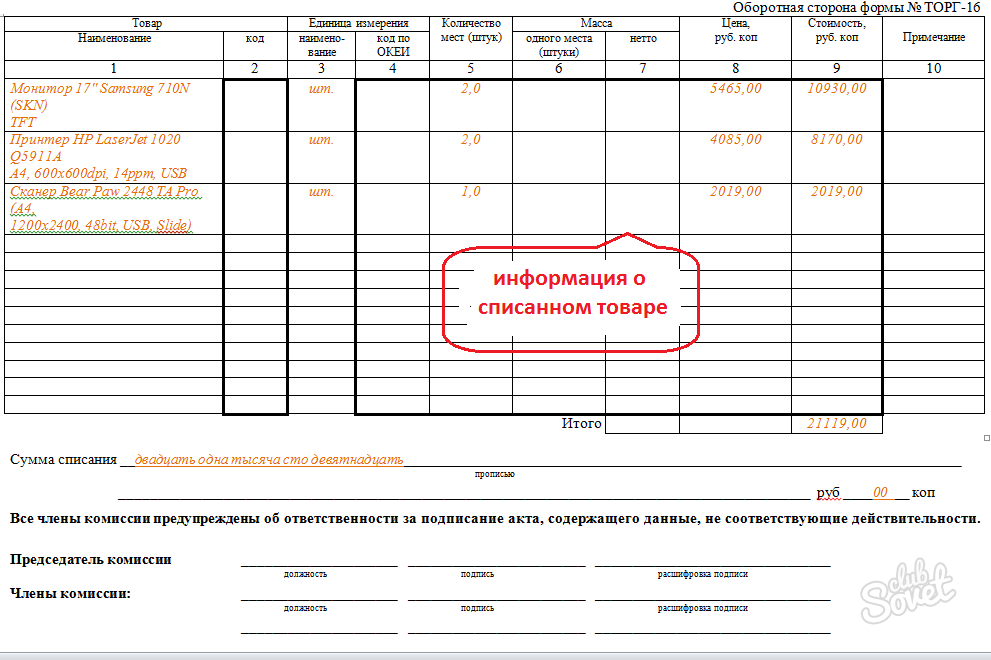

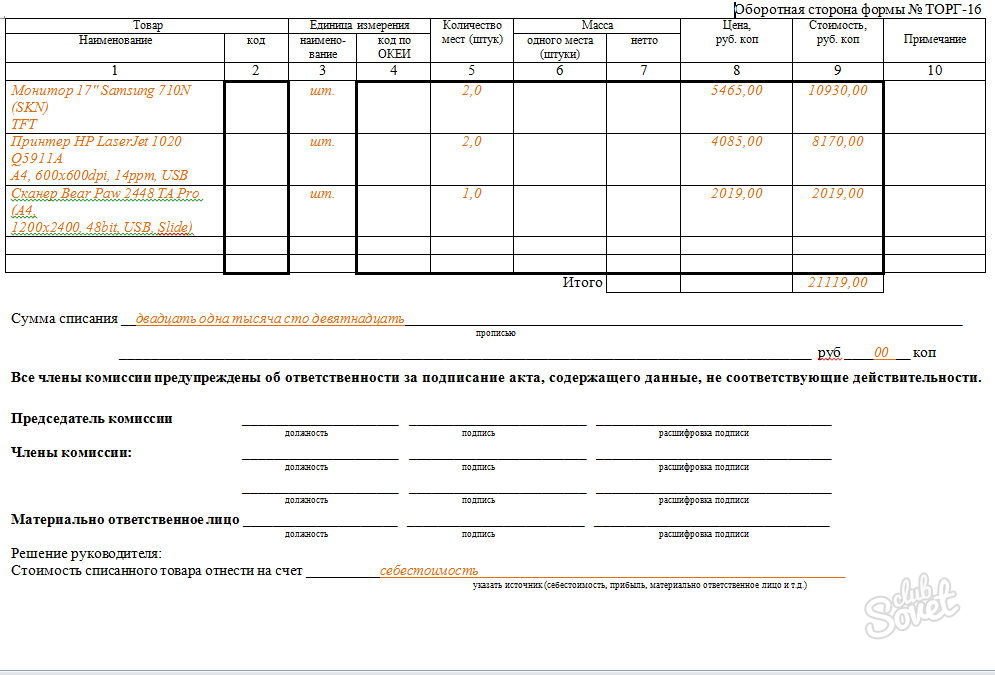

The main part of the document is a description of the goods and materials being written off. Full information about them can be arranged for convenience in tabular form. The table contains the following columns: product name, inventory number, unit of measure (for example, “piece”), quantity, cost of this product, total amount of all units, reason for write-off. At the bottom, the total book value and write-off amount are summarized.

The act is certified by the signature of the chairman and all members of the commission, again with a full name and an indication of the position held. Sometimes appendices are provided for the act. They are listed before signatures. The seal of the organization is put, the date of signing the act. After that, the write-off act is submitted to the head of the organization for approval.

The document is made in 3 identical copies. A copy remains in the accounting department, the second is transferred to the head of the department that wrote off the inventory, the third is given to the financially responsible person. The head can write a resolution to recover the amount of damage from the financially responsible person if the damage to the goods occurred due to his negligence. For example, "Recover loss due to damage to goods from ...".

Useful documents:

The write-off act serves to make an appropriate entry in the accounting books, the basis for the disposal of material from the balance sheet of the enterprise. Before drawing up a write-off act, make sure that the goods being written off are issued from the warehouse on demand. Representatives of sanitary supervision may take part in the signing of the act.