What is the Unified Social Tax - objects, subjects of taxation and the abolition of the UST

Familiar to all owners of summer cottages and cars. Income tax is paid by all working citizens, but they may not know what UST is.

What is the unified social tax

In the very name of the UST, its essence is encrypted - it is a social tax. The abbreviation UST stands for single social tax. These are deductions aimed at mobilizing funds intended for pension and social security at the state level.

These tax levies were not deductible from the working population, the UST was paid at the expense of funds and organizations. The tax rate was the same - 26% of the wage fund. These amounts were not deducted from wages, the workers themselves paid a different tax.

New taxes instead of UST

The unified social tax was abolished from 01.01.2010. Now payments for the same purpose are supposed to be made to three state organizations. These are 3 different structures:

- Pension Fund of the Russian Federation (PFR).

- Social Insurance Fund of the Russian Federation (FSS).

- Compulsory Medical Insurance Fund of the Russian Federation (FOMS).

At first, the combined rate for these 3 funds was identical to the UST, but in January 2011 there was an increase in payments to 2 funds at once. Later, the percentage of payments was slightly reduced, but they did not equal the previous 26%, after reducing the total rate of social taxes - 30%.

This video will tell you what deductions are included in the unified social tax:

Regulatory regulation

The legal regulation of the UST was formalized at different levels.

- The obligatory nature of social taxes is provided for in the Constitution of the Russian Federation. It is this document that is the main one, occupying the first level of legal acts.

- Also in the first level are the Labor (TK), Tax (NK) and Civil Codes (CC) of the Russian Federation.

- Federal laws also belong to the first level of regulation. The unified social tax was introduced on January 1, 2001 in accordance with Federal Law No. 118 of August 5, 2000. In this form, social tax payments lasted 9 years. According to Federal Law No. 212 of July 24, 2009, the UST was replaced by other payments, starting from January 1, 2010.

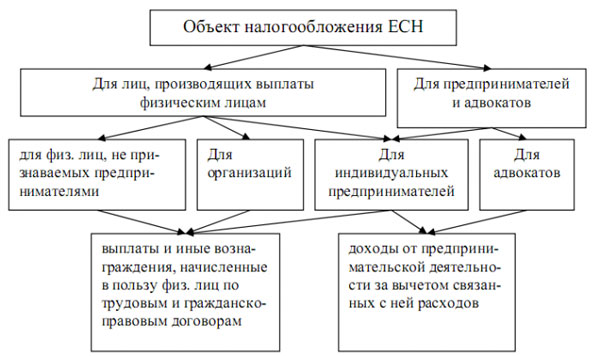

Objects of taxation

- Under objects of the unified social tax of the first group income under employment contracts of various nature and payments under one-time contracts were understood. The UST was also levied on remuneration under civil law contracts that imply payment for services or the performance of any work with a certain income. Contracts for or property were not objects of UST taxation.

- The second group of UST objects also implies income, but it refers to private practice. This is the remaining funds after deducting expenses in the conduct of a private business or professional activity of a different nature.

There were also tax benefits, a whole category of income was exempted from paying the UST:

- Payments under personal voluntary insurance contracts

- Tax-free government compensation and benefits

- Compensation upon dismissal for vacation not used during work

- Insurance premiums under contracts for voluntary medical insurance for their employees.

UST objects

The amount of objects of taxation was determined by periods.

- The classic tax period was allocated for a period of 1 calendar year.

- There were also 3 reporting periods - 1 quarter, half a year and the first 3 quarters of the year.

Legal advice on the return of UST is given in this video:

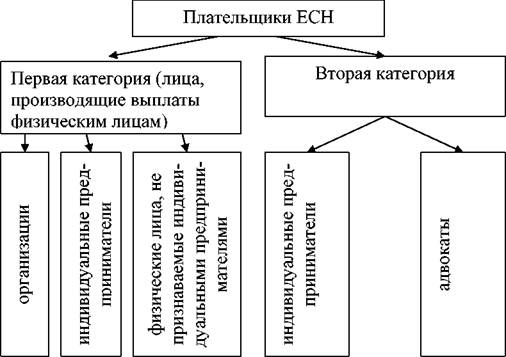

Subjects

Payers of the unified social tax were divided into 2 groups.

- First were entities with employees receiving wages, regardless of whether the activity is carried out by an individual entrepreneur.

- To the second group included individuals in private practice. These include lawyers, notaries, and other self-employed taxpayers. Often such entities were also payers of the first category in parallel - they were taxed for private practice and for paying salaries to hired employees. An example would be an administrator in a doctor's office or a secretary at a notary.

Subjects of the UST

Important nuances

In 2017, once again they started talking about the return of the UST. Initially, it was introduced to simplify tax calculations, allowing you to submit documents and transfer funds to one organization. In 2010, it was decided that this was unprofitable in terms of tax collection, so the UST was divided into 3 funds. Now the issue of returning to the taxation model in the UST format is still open. An active discussion on the return of this system began in 2016, although in 2015 it was decided not to resort to the payment of social taxes in the UST format.

The concept of a single social tax has been outdated for several years, but even accountants still call UST payments to 3 state bodies. It doesn't matter what the social tax payments are called - they go towards providing pensions and other government benefits.

Theoretically, a return to the UST is quite possible, this measure is now being considered by the government as an anti-crisis measure. This will be clear by the middle of 2017, but if the UST is returned, then an increase in the rate for people with high wages is already provided. So far, an amount exceeding 796 thousand rubles of earnings per year has been announced.

It remains only to wait and find out whether the UST will actually be returned.