Acts of reconciliation of mutual settlements: sample. How to make a reconciliation act?

Clear control, keeping accurate records and strict control over the conduct of economic activities are the basis for the fruitful and calm work of the enterprise (individual entrepreneur), as well as the absence of disagreements with counterparties.

To achieve these goals, the act of reconciliation is used.

Reconciliation act as an accounting document

Reconciliation acts are an accounting document that displays mutual settlements for a certain period of time between two legal entities or individual entrepreneurs. At the legislative level, this reconciliation act is not regulated in any way, since it is not a primary document.

Nevertheless, most accountants prefer to have a signed act in their arsenal. With its help, you can resolve disputes that arise between counterparties, as well as protect the interests of a particular enterprise (individual entrepreneur), including in court.

In order for such a document to have the form and content of real evidence, some norms of the current legislation, as well as established judicial practice, should be taken into account when drawing up it.

This accounting document plays an extremely important role in the following situations:

- with a wide range, which is offered by one seller;

- in case of granting on the part of the seller of a delay in payment;

- at high cost on the range of goods or services offered;

- if there is a relationship between counterparties on a regular basis;

- to simplify accounting and control at the enterprise(from an individual entrepreneur) if the latter has a large number of concluded contracts or other agreements.

Due to the fact that there is no fixed form of the reconciliation act in the current legislation, enterprises are allowed to develop a sample document at their own discretion.

Moreover, the Ministry of Finance insists on this in letter No. 07-05-04 / 2 signed on February 18, 2005.

But at the same time, based on a systematic analysis of existing regulatory legal acts, there are two main requirements that must be met when forming acts of reconciliations of mutual settlements:

- this document must be drawn up in two authentic copies, one for each party who signs it;

- on the part of the enterprise, only the director or the chief accountant has the right to sign, and their signatures must be sealed.

As it has already become known, the form of the act of reconciliation of mutual settlements can be developed independently. However, established practice suggests that when drawing up an act, one should include in it those data that should be inherent in all primary documents.

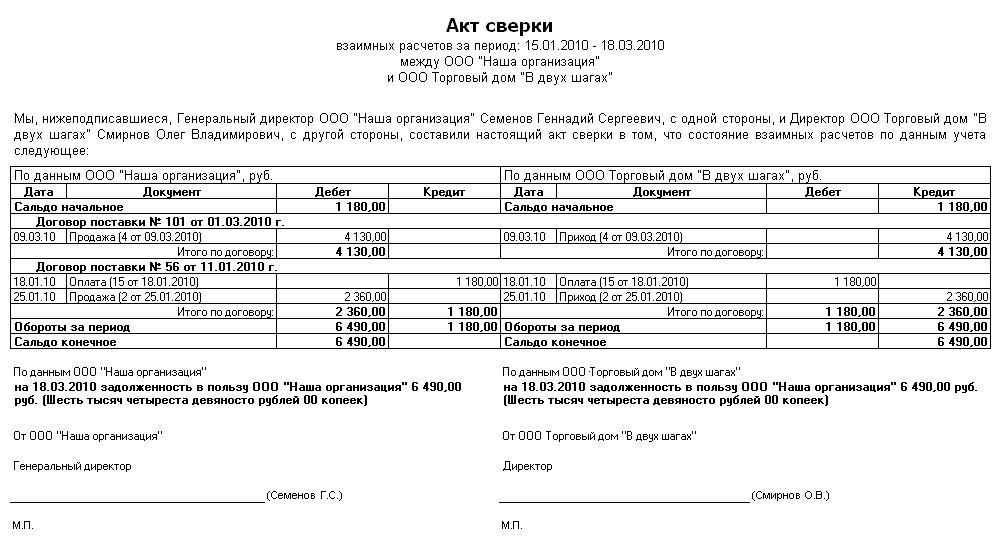

Based on this, the act of reconciliation of mutual settlements must have:

- outgoing number;

- date of signing;

- the period for which reconciliation is carried out;

- name of contractors;

- indication of the full name of the official who signs the act;

- a table that indicates data on debit and credit, information on deliveries, calculations made and existing debts;

- balance at the beginning of the period for which the act is drawn up, as well as at the end of the period;

- data on the total turnover;

- a duplicated table without data, to provide the counterparty, if there are discrepancies, to indicate their data.

The signed act of reconciliation indicates that the parties confirmed the existence of a relationship between them, and also indicated accurate data regarding the actual state of mutual settlements.

In addition, it indicates, if any, debt obligations, as well as the lack of full settlement. It is these data that act as an argument in favor of a particular person when he goes to court in order to avoid the process of proof.

The signed act of reconciliation is a weighty evidence during the period of litigation. In addition, during the period of pre-trial settlement of the dispute, this document indicates the fact of recognition by the party of debt obligations.

From all of the above, we can conclude that there is no obligation to maintain an act of reconciliation of mutual settlements at enterprises and individual entrepreneurs.

However, thanks to the data recorded in them, it is possible to avoid accounting errors, maintain full control over economic activities and avoid disputes between enterprises (individual entrepreneurs), as evidenced by the practice established by federal arbitration courts.

Noskova Elena

I have been in the accounting profession for 15 years. She worked as a chief accountant in a group of companies. I have experience in passing inspections, obtaining loans. Familiar with the areas of production, trade, services, construction.