The act of writing off material assets: a sample of filling out the form, download the form

Any person, wherever he is and whatever his nationality, has material values. It can be clothes, household items, appliances, etc. Likewise, legal entities have inventories on their balance sheet. The difference lies in the fact that if an ordinary person can simply throw out a spoiled or unnecessary thing at any time, then an organization or a private entrepreneur must write it off correctly.

Damaged inventory items may be found during their operation by company employees or as a result of an inventory. In the latter case, lost values are often revealed. If damaged, obsolete or lost goods and materials are found in an organization or enterprise, then a special commission should be created that will assess the condition of these values and draw up an act on their write-off, if necessary. The commission must necessarily include people financially responsible for the values in question, as well as their leaders. In this case, goods and materials must be written off using a special act.

The main reasons for write-offs are:

- valuables have fallen into disrepair due to long-term use;

- may be damaged or broken by accident. For example, the dishes in the dining room may simply break;

- may be lost;

- they are morally obsolete. This applies mainly to technology, such as computers, printers, etc.

Ultimately, the act is necessary so that the accounting department can write off the inventories indicated in it. The form of the act for the write-off of material assets in any organization can be drawn up independently.

However, there are certain rules that must be observed:

- The document must be drawn up in two copies. One of them is stored in the accounting department, so that in case of verification it can be presented. The second is kept by the financially responsible person. If this is a warehouse, then most often it is one of the storekeepers.

- The commission, in addition to the above persons, must necessarily include the chief accountant and the head of the warehouse, if the goods are in the warehouse.

- Members of the commission must be appointed by the head of the enterprise, for which a special order is issued.

At each enterprise, an inventory is regularly carried out, as a result of which goods and materials to be written off are identified.

What is an act

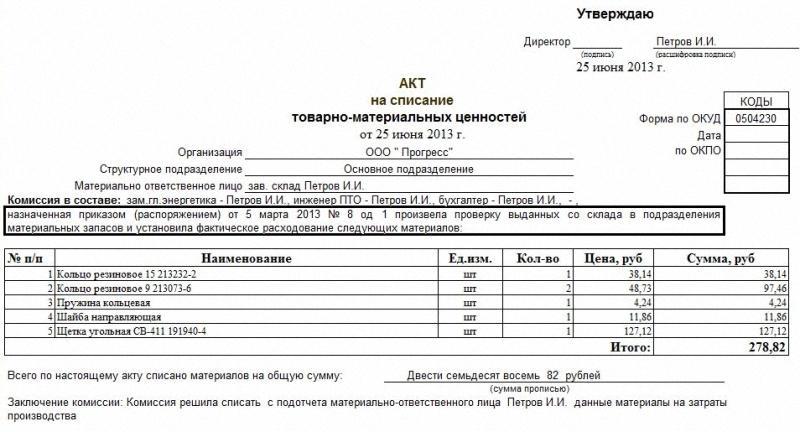

As mentioned above, there is no single state-approved form of a write-off document. It can be developed independently in a form convenient for the enterprise. You can download the form of the inventory write-off act on our website. In any case, it must contain some mandatory elements. These include:

- names and positions of members of the commission, as well as their signatures, after the inspection and decision;

- in fact, the decision that was made;

- date of inspection of valuables;

- list of considered values and their value;

- the reasons why they were declared unusable and subject to write-off;

- the total amount of goods and materials to be written off.

Note: if the write-off is carried out according to the results of the inventory, then it is necessary to indicate in the act that the valuables were lost, which is confirmed by the results of the inventory. This will be the reason for the cancellation.

It is convenient when the document is drawn up in the form of a table, in the first column of which the name of the values \u200b\u200bto be written off is entered. Further, in subsequent columns, their quantity, cost and reason for writing off are filled in. It is convenient to draw up such a form both on a computer and manually. At the end, the document must be signed by all members of the commission and must be approved by the head of the enterprise. Only after that it can be transferred to the accounting department.

Features of compiling a document

When a company is engaged in the production of products or the construction of buildings, then part of the inventory is simply spent . In accounting, their value is transferred to the cost of the products received, but in order to do this, it is necessary to draw up a write-off act. This is done in order to record the fact that the materials were used up. However, not everything is so simple here. First of all, it is necessary to determine the cost at which the values will be written off. In principle, this should be spelled out in the company's even policy. In addition, before drawing up an act of writing off materials for production and construction, it is necessary to actually ship them from the warehouse, for which a consignment note is drawn up.

In the act itself, it is necessary to prescribe the cost of each type of materials written off and their quantity. Calculate subtotals and totals. All this is done on the basis of the method of calculation adopted in the accounting policy. A sample of drawing up an act for the write-off of goods and materials can be downloaded from.

For the drafting of this act, there is no need to collect a commission, but the presence of a materially responsible person is still mandatory. First of all, the person responsible for the materials must provide a report on what materials have been transferred to production. Confirm the data of the report must be waybills.

Second reason to draw up a write-off act is the calculation of the cost of products manufactured by the enterprise. It indicates the amount of materials needed to produce a unit of output.

The third reason is the report about how many products were produced in a certain period. Thus, the person responsible for drawing up the act will be able to calculate the total amount of write-off.

An act for the write-off of goods and materials is drawn up so that the accounting department can write them off, since they were spent in the production process

Features and nuances of write-offs

At first glance, it may seem that the procedure for writing off inventories is quite simple. However, it is not. There are some nuances that need to be taken into account. If the values are written off to production, then their cost is written off:

- at the real cost of the acquisition, if it is known for each specific unit of goods (which is relevant when single materials are written off);

- at some average price;

- at the price at which either the first or the last materials arrived.

Note: an important nuance is the write-off of goods and materials in public institutions. If items of equipment or furniture are written off, then it is imperative to pay attention to the year of their release.

There are specially developed standards that indicate the service life of various items. This is necessary so that, in the event of an audit, you do not get charged with theft of state inventory. The State Commission will check whether this product was really subject to write-off. Therefore, do not rush to dispose of decommissioned items.

The act of writing off material assets, a sample of which can be downloaded on, has no features when executed in public institutions. No specific form of act is established by law. In addition, it does not prescribe methods for the destruction of decommissioned valuables. Disposal of decommissioned items is carried out at the discretion of the head of the enterprise. They can be thrown away, burned, given to another institution.