The act of writing off material assets: what is it, sample, form

Commodity-material assets (TMC) name the funds that were acquired at the expense of the enterprise. They can be used to create ready-made products, carry out labor activities and meet the needs of an organization or enterprise. In the process, some materials may be deemed unsuitable. Then they need to be written off.

- .word

- .Excel

It is impossible to keep correct intra-company accounting without drawing up an act of writing off material assets. On the basis of a correctly executed document, a certificate is prepared on the change in inventories in the accounting system.

The accounting policy does not provide for the formation of a single sample of the write-off act. Each specific organization must form a form in accordance with the norms of office work and the individual needs of the enterprise.

The document must be drawn up in two copies:

- One of them is kept by the materially responsible employee.

- The other is in accounting.

Usually, the write-off procedure is carried out by a special commission, which operates on a temporary or permanent basis.

The commission must necessarily consist of persons who are financially responsible for certain values of the organization. Members of the commission have all the powers to draw up a write-off act. After the formation of the act, it is signed by the commission and submitted for review to the head of the enterprise. When drawing up a document, a standard sample of an act can be used.

The commission should include:

- Chief Accountant.

- Persons who are financially responsible for the specified values.

- Specialists in a specific profile, if professional equipment is subject to write-off.

The composition is mandatory appointed by the leadership of this organization. After the commission, the accountant should reflect the book value of the written-off material assets and the extent of their damage. Entries are made on the basis of a previously drawn up act. If the guilty persons are involved in the write-off, it will be necessary to make calculations to compensate for the material losses of the enterprise.

The write-off may occur as a result of a natural disaster. But then you will need not only a write-off act, but a certificate from the accounting department in the form.

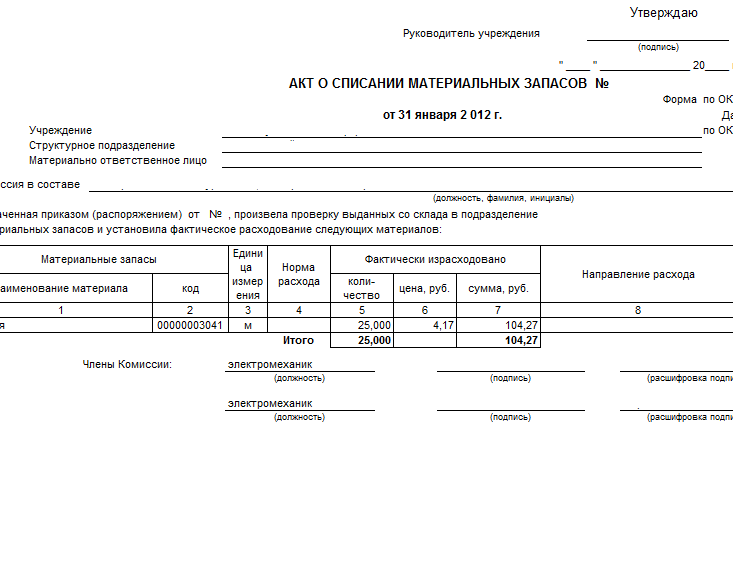

An act for the write-off of material assets is drawn up in a form convenient for a particular enterprise. But it must contain the following information:

An act for the write-off of material assets is drawn up in a form convenient for a particular enterprise. But it must contain the following information:

- Place and date of the document.

- List of members of the write-off commission in alphabetical order and positions. The name of the chairman must be listed first.

- Information about material assets (name, quantity and units of measurement, cost of materials prepared for write-off).

- The reason for the marriage (the unsuitability of materials).

- The total cost of written off material assets.

It is recommended to arrange the main part of the document in a tabular form or a list for greater clarity and convenience. At the beginning of the act, the date and title are written. Then follows a confirmed fact on the basis of which the commission acts. The number and date of the order previously signed by the head of the enterprise must be affixed.

The stamp of approval can be affixed in the upper right corner of the act and only on the first page. This is a mandatory rule for any institution, regardless of the type of material assets. At the conclusion of the act, all members of the commission must put their signatures. It is also required to put down the position and decryption of the signature for each member of the commission. Be sure to indicate the date of signing this document on the very last page. Without one of the specified points, the write-off act will be considered invalid.

In order to reduce the time spent on writing off material assets, you can create a commission of one person - the chief accountant. But the head of the enterprise must approve the expediency of making such a decision.

If the company is engaged in construction activities, the procedure for writing off materials will have its own specific nuances. Consumption norms are spelled out in the design and estimate documentation and laid down at the initial stages of construction.

To calculate the volume of materials that was used in the construction of the facility, specialists from the production and technical department are involved. The cost of written-off material assets is indicated in the document without fail. In this case, you need to take into account:

- Payment for consulting services.

- The cost of intermediary services.

- Customs costs.

- The cost of materials at the time of their purchase.

- Transportation costs that were associated with the loading of materials and delivery to the warehouse with subsequent unloading.

For the correct construction of the workflow for the write-off of materials in the construction industry, it is necessary to adhere to the following established scheme:

- At the very beginning of the billing period, an inventory of the goods is carried out in the warehouse, that is, its recalculation. It is important to determine the volume of stocks and generate a report for the heads of production sites.

- By the end of the reporting period, the site manager must correlate the actual consumption with the information received and send this data to the technical department. His report is compiled on the form M-29.

- The PTO checks the documents and sends them to the engineering department.

- The information received is rechecked again and given to the accountant for the final determination of the amount of income and expense, as well as the balance. Then a summary sheet is formed.

The commission for writing off materials must necessarily include: an accountant, an engineer of the technical department and a chief engineer.

As for the document in the M-29 form, its first section indicates the rate of required materials and the amount of work performed. In the second section, costs are compared with production volumes (in tabular form). The bill of lading, the order of consumption of building materials in writing - these are the documents that are taken into account when forming the document.

Act on the write-off of materials into production: features of drafting

If it is necessary to draw up an act on the write-off of material assets for a manufacturing enterprise, it will be necessary to remove the used resources from the warehouse even before preparing the document on the demand-invoice.

If it is necessary to draw up an act on the write-off of material assets for a manufacturing enterprise, it will be necessary to remove the used resources from the warehouse even before preparing the document on the demand-invoice.

Fixing the fact of the consumption of inventories is the main goal of write-offs in production. You can determine the real cost, which will then be displayed in the corresponding document, in different ways. Here are some of them:

- According to the cost of materials that arrived first or last by the time the act was formed.

- Within a particular category of materials, their average cost is determined. The total cost is divided by the number of units, and the desired indicator is obtained.

- If it is necessary to evaluate a particular valuable resource, this is done for each unit separately.

For the correct preparation of the write-off act, you need to prepare the following documents:

- Report of the materially responsible person on the used material stocks.

- Reports on the number of products created for a certain period of time.

- Planned costing, where all the main costs for the production of one unit of output should be listed.

The form of the write-off act should be developed by the accounting department, taking into account the peculiarities of the production process at a particular enterprise.

After drawing up the document and recognizing a number of materials as written off, the accountant should make the following entries:

- D94 K10. It should reflect the book value of the written-off materials. The necessary data can be taken from the act itself.

- D20 K94. In posting in this form, it is necessary to reflect the cost of shortage or damage to materials in the redistribution of maximum loss. Information can be obtained from the write-off act and a special accounting statement. If the natural loss limit has been exceeded, instead of an account in the D20 form, additional sub-accounts will have to be drawn up.

In some cases, accounting will have to use other postings. For example, damage to material assets could occur due to a natural disaster. Then they make the wiring D99 K10. If a gratuitous use agreement was applied, postings D91/2 K10 and D91/2 K68 are generated, that is, VAT.

In some cases, accounting will have to use other postings. For example, damage to material assets could occur due to a natural disaster. Then they make the wiring D99 K10. If a gratuitous use agreement was applied, postings D91/2 K10 and D91/2 K68 are generated, that is, VAT.

Competent and timely drawing up of a write-off act can significantly simplify some procedures and protect an enterprise from thorough tax audits.

But in some situations, preparation for drawing up an act and its direct formation take too much time. In such a situation, the management of the organization may refuse to draw up an act on the write-off of material assets. But doing this is highly undesirable. Ultimately, special invoices will be required. This process will not be as productive. But it does not require the collection of a separate commission.