The act of writing off valuables

A correctly and timely drafted act of writing off valuables can mean facilitating the procedure for passing tax audits of an organization, as well as competently keeping accounting records. Violation of which, by the way, can become the basis for bringing to administrative and even criminal liability. This document is compiled necessarily, like others. Only it is not personnel, but accounting.

The document in question aims to record the consumption of material assets that can no longer be used in the organization. These are fixed assets, and inventories, goods and other enterprises accounted for by the accounting department.

The specifics of drawing up an act of writing off values is that there are several approved and recommended forms of such documents. What form to use, whether they are mandatory for use - you will find all the nuances in this article.

Download sample:

(14.5 KiB, 974 hits)

An example of an act of writing off values

I approve:

CEO

Vostok PromTeh LLC

Minokhin V.K.

August 04, 2017

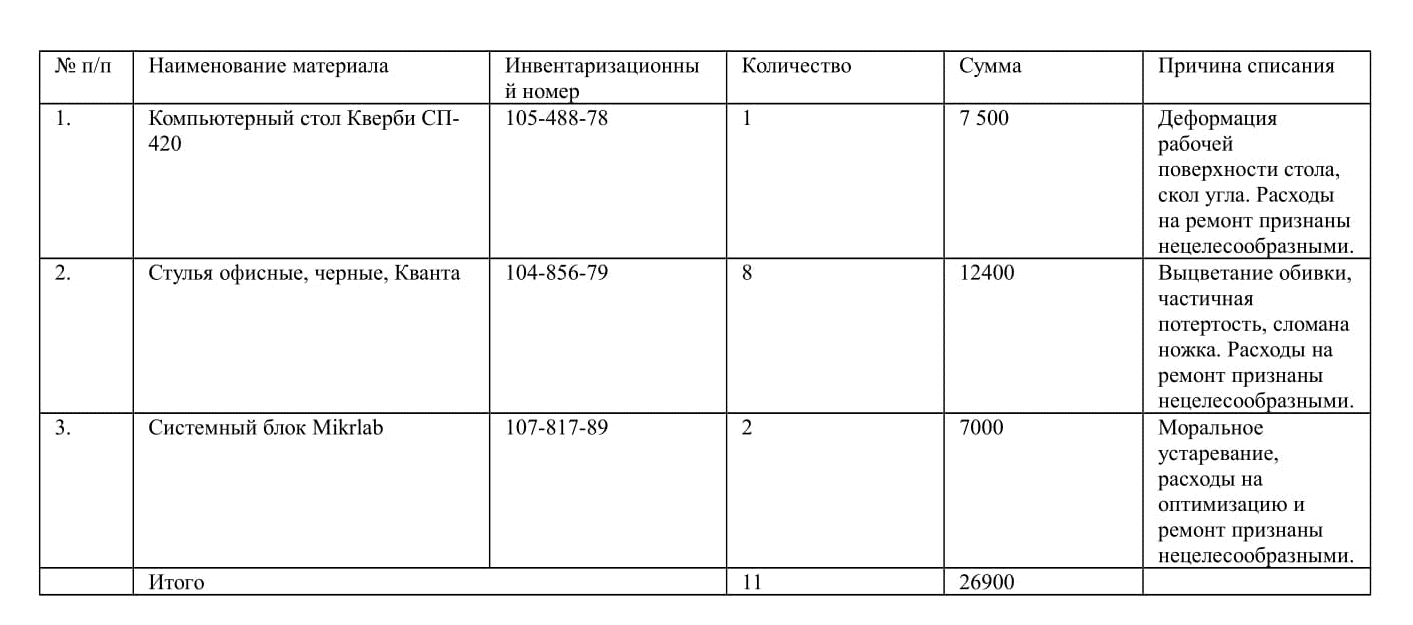

Act of write-off of valuables No. 1

August 04, 2017

Commission consisting of: chief accountant Prokopenko Igor Vladimirovich, storekeeper Stepanov Konstantin Fedorovich, executive director Osipov Dmitry Konstantinovich, programmer Stukov Alexander Vladimirovich,

acting on the basis of the order of the General Director of the Company No. 49 dated May 3, 2017,

wrote off the following inventory items due to their unsuitability for further use:

Total 11 units. for a total amount of 26 900 (twenty six thousand nine hundred) RUB.

Commission members:

chief accountant Prokopenko I.V.

storekeeper Stepanov K.F.

executive director Osipov D.K.

programmer Stukov A.V.

Types of acts of writing off values

Accountants know that the legislation of the Russian Federation provides for several unified forms of write-off of inventories. So, for the write-off of spoiled, expired, defective goods and food, the TORG-16 form is provided. Order of the Ministry of Finance of Russia dated March 30, 2015 No. 52n introduced the form of the Act on the write-off of inventories. For fixed assets of an enterprise, the Ministry of Finance has developed unified forms OS-4 (one object), OS-4a (vehicles), OS-4b (a group of fixed assets).

Is it obligatory to use these forms to write off valuables to private organizations and individual entrepreneurs? From January 01, 2013, such forms are not mandatory. The head has the right to independently determine the form of documents used to formalize the facts of economic life. At the same time, in order not to raise questions from the tax authorities, acts of writing off valuables must contain a number of mandatory details.

We draw up an act of write-off of values

The document must be drawn up collectively. This may be a permanent or temporary commission created in accordance with the order of the head. It includes an accountant, a financially responsible person, a warehouse worker and other employees at the discretion of the management.

So, what details are mandatory for the act of writing off values? Since this document is of fundamental importance for accounting, the Accounting Law provides for the following elements:

- name of the document (act of write-off of valuables, act of write-off of goods, act of write-off of goods and materials, etc.);

- date of the document. According to the accounting rules, the act must be drawn up at the time of the economic act or immediately after its completion;

- name of company;

- members of the commission by last name, indicating the position;

- name of value, article, quantity or weight, cost, reason for write-off;

- signatures of committee members.

Since the act of writing off valuables is an accounting document, it is approved by the head and signed by the chief accountant of the organization.